-

- Author

- J. Phil Buchanan

-

- Published

- January 12, 2026

Articles

The Billion-Dollar Blindspot: How Process Widens the Revenue Gap

US banks are hemorrhaging billions in revenue from their most profitable client segment: business owners. The issue isn't a lack of talent, technology, or resources, but from cultural architecture designed for product silos, not relationship economics. While banks invest heavily in commercial lending, private banking, and wealth management capabilities, these divisions often operate with processes that systematically fragment the client experience — driving business owners to consolidate with competitors who demonstrate superior integration. This whitepaper examines why banks, despite being naturally better positioned than any other financial institution to serve business owners comprehensively — are losing ground to smaller, more agile competitors. More importantly, it provides a roadmap for senior executives to transform their organizations from fragmented service providers into integrated partners that capture the full lifetime value of their most profitable clients. The transformation required isn't technological or structural — it's cultural. Senior leaders who recognize this reality and act decisively will capture competitive advantages that compound over decades. Those who don't will continue losing their most profitable relationships to competitors who already have.

US Banks Are Losing Billions Due to Process Failures

Not because of a lack of talent or technology - but because they're executing the wrong processes for serving business owners.

Fragmented Service Is Driving Clients Away

Despite having the capabilities, banks lose ground to smaller competitors by operating in silos instead of delivering holistic, integrated service.

Culture, Not Technology, Is the Key to Transformation

The path to capturing lifetime client value lies in cultural change led by senior executives - not in new tools or organization charts.

The $250 Million Wake-Up Call: A Process Failure Case Study

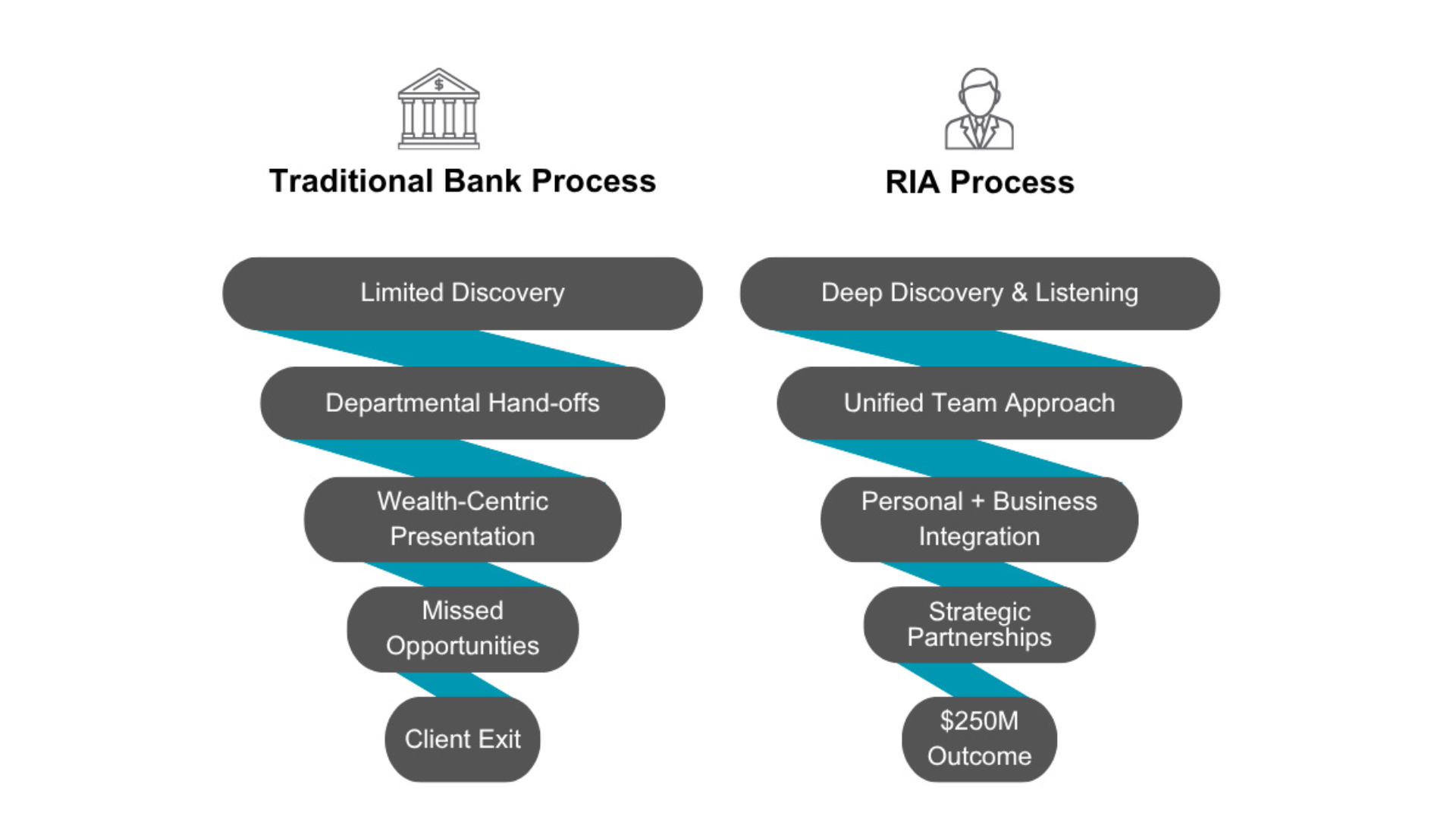

Before we examine what banks should be doing, let's look at what happens when they get it wrong. This real-world example illustrates the catastrophic cost of process failure — a story that plays out in banks across America every single day. A highly successful business owner spent 25 years as a loyal commercial client of a well-known US bank. Over that quarter-century, he borrowed and repaid over $83 million in commercial loans while utilizing comprehensive depository and treasury services for domestic and international operations. The bank had complete visibility into his success through the required documentation, including corporate and personal financial statements, tax returns, and detailed business plans. As his wealth grew, the bank's process kicked in. The commercial banker made referrals to the private wealth management group, following the documented procedures perfectly.

The First Failure

The initial wealth management meeting followed the bank's standard process. The advisor spent most of the session explaining "how we help busy business owners manage wealth" without clearly understanding the client's unique situation. The presentation was polished, professional, and completely product-focused. No meaningful discovery occurred. No insightful questions were asked. The advisor pitched services based on assumptions rather than insights. The business owner's response to his commercial banker was swift and definitive: "Never bring that individual back."

The Second Failure: Insanity Defined

Years later, the commercial banker convinced the client to try again by doing him a "favor". While the advisor changed, the process remained the same. The experience was virtually identical — another product-centric presentation devoid of client intelligence about the client's real needs, goals, or circumstances: Strike two. The commercial relationship was effectively over, though it would take years to fully play out. While the bank viewed the client through the lens of their siloed business segments, the client viewed their business, wealth, and legacy as one inseparable whole. The business was their retirement. Their personal legacy was their company. To the business owner, it was all one life, but the bank refused to see it that way.

The Competitor's Different Process

Meanwhile, the business owner began working with a Registered Investment Advisory firm. The difference in approach was immediately apparent. These advisors made it about him and his biggest needs. They asked probing questions, listened actively, and invested significant time understanding far more than just his finances. They were determined to learn about family dynamics, personal goals, business endeavors, and vision for the future before ever mentioning their capabilities. The discovery process revealed opportunities the bank had never identified despite 25 years of financial intimacy. The RIA helped consolidate fragmented investment relationships, optimize the family foundation structure, perfect long-term estate planning, and develop comprehensive wealth legacy strategies. More significantly, the RIA introduced the client to specialized partners, including a private credit firm. This relationship ultimately led to restructuring $17 million in debt, completely replacing the bank's commercial lending relationship.

The $250 Million Finale

Two years later, the business owner successfully sold his company for more than $250 million through a capital markets firm recommended by the RIA. None of the proceeds stayed with his original bank. A quarter-century relationship that should have generated tens of millions in fees across multiple divisions produced zero dollars from the most significant financial event in the client's life.

The Painful Truth

The bank didn't lack capability. It had all the right units: business succession specialists, experienced wealth managers, sophisticated capital markets professionals, and so forth. The bank had a well designed and documented process that should have captured this opportunity. What the bank lacked was a culture that prioritized genuine client discovery over departmental handoffs. The bank's process was designed for internal efficiency, not client experience. Every interaction was filtered through departmental perspectives rather than the client's comprehensive needs. The business owner walked away to prosper from a unified team that earned his trust and delivered integrated solutions. The bank was left with a $250M loss that cost more than revenue — it destroyed 25 years of relationship equity and exposed a cultural flaw the executive team couldn't see from inside their own organization. This is the kind of situation that is eerily reminiscent of Warren Buffett's prophetic quote: "It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you'll do things differently." All the goodwill built up and developed by the commercial lender was gone. This isn't a unique story. It's happening right now in banks across the country, with business owners who represent similar lifetime value potential. The only question is whether senior executives will recognize the pattern and act before more relationships disappear.

The Billion-Dollar Question: What Does Serving Business Owners Holistically Actually Mean

Before we can fix the process problem, we must clearly define what comprehensive service looks like. Serving business owners holistically means recognizing that successful entrepreneurs don't compartmentalize their financial lives — and neither should banks.

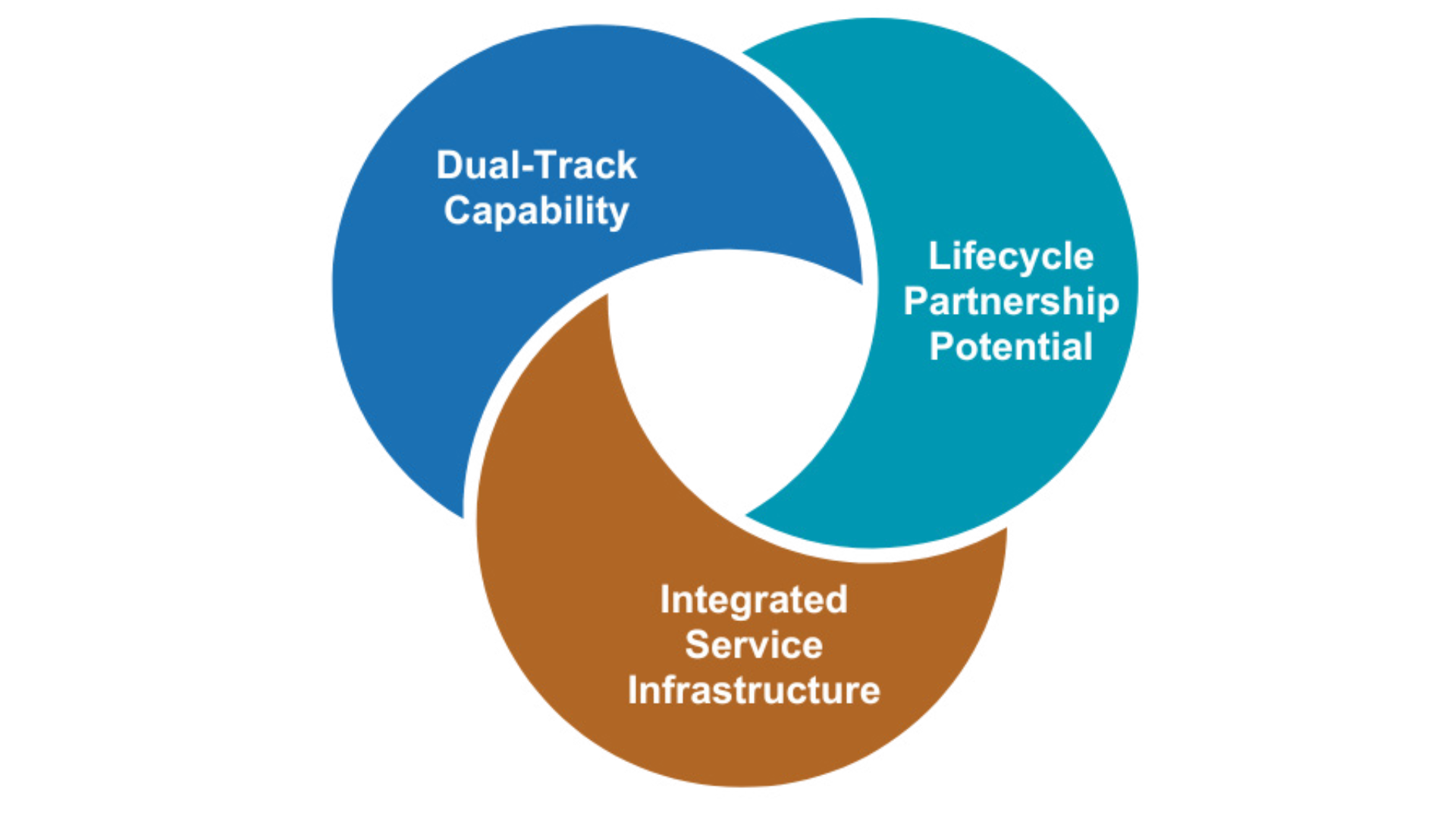

The Natural Advantage Banks Are Squandering

Banks possess unique advantages that position them as the ideal comprehensive financial partners for business owners:

- Dual-Track Capability: Banks can serve clients both personally AND professionally, understanding the intricate connections between business cash flow, personal wealth accumulation, and family financial goals.

- Lifecycle Partnership Potential: Banks are uniquely equipped to support business owners through every stage of their entrepreneurial journey — from startup capital to succession planning — while simultaneously addressing personal financial milestones.

- Integrated Service Infrastructure: Unlike independent advisors who must coordinate with multiple institutions, banks can provide seamless integration across commercial lending, treasury services, wealth management, and private banking. Yet despite these natural advantages, banks consistently lose business owners to more nimble competitors who understand one fundamental truth: business owners don't want to be handed off between departments; they want to be understood by a unified team.

The Business Owner Lifecycle: A Framework Banks Must Master

Just as consumer banking segments have embraced “Ages and Stages” planning and “Client Journeys” for families, so must banks develop sophistication around the business owner lifecycle. These frameworks reveal why process transformation is so critical. Below is a partial example of how integrated strategy and lifecycle thinking apply to business owners.

The Cross-Stage Crisis Reality

Business owners don't progress linearly through these stages. They face cross-stage crises that require immediate, comprehensive support: economic downturns requiring emergency capital, supply chain disruptions causing cash flow challenges, liability exposures threatening both business and personal assets, key person departures disrupting operations, and family crises affecting business continuity. Many entrepreneurs simultaneously operate multiple businesses at different lifecycle stages, adding another layer of complexity. They might have one mature business requiring talent retention strategies while launching another venture needing startup capital and establishing employee benefit programs for a third entity.

The Data Confirms the Problem is Systemic

Recent research from Coalition Greenwich reveals the scope of this process failure: more than 50% of small and mid-sized business owners report their primary bank has never discussed private banking or wealth services with them. Yet 42% of small-business owners and 50% of mid-sized company executives would definitely consider using their commercial bank for wealth services if approached properly.

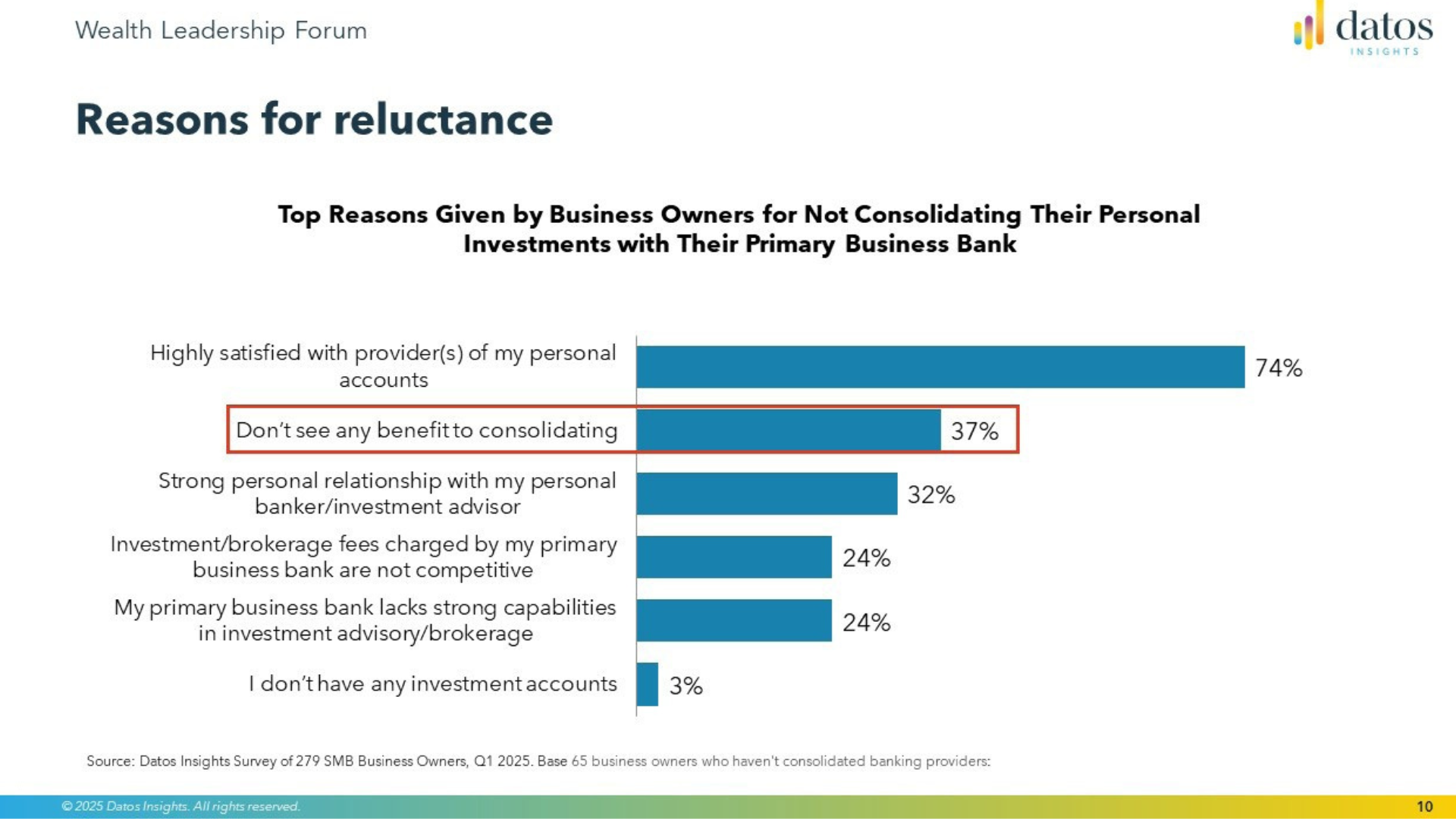

According to Deloitte, consumer expectations for seamless banking experiences are rising, but business owners encounter fragmented reality at every touchpoint. The window to fix this before competitors capture these relationships is closing rapidly. Perhaps most revealing is what business owners say when asked directly why they don't consolidate their personal investments with their primary business bank. The data exposes the heart of the process failure (see Figure 4). These responses reveal the challenge: 74% satisfaction with current providers isn't a testament to competitors' superiority — it's evidence that banks have failed to create any basis for comparison. Business owners aren't choosing other providers because they're better; they're staying with them because their banks haven't given them a compelling reason to consider consolidation. The 37% who 'don't see any benefit' represents the most damaging indictment of current banking processes. These business owners work with institutions that have complete visibility into both their business and personal financial situations, yet bank colleagues lack the strategic, holistic vision, conversational competence, storytelling ability, and discovery skills to help clients recognize the integrated value they're missing.

The Silo Effect on Client Experience

Current banking processes create predictable failure patterns. Commercial teams focus on credit metrics and capital deployment with transaction-focused, renewal-driven, compliance-heavy interactions. Wealth teams concentrate on assets under management and investment performance through investment-focused, meeting-scheduled, product-driven engagements. Private banking teams tackle deposits, liquidity management, everyday banking, and credit facilities via service-focused, reactive, accommodation-oriented touchpoints. Treasury management professionals are focused on ACH issues, fraud detection, and efficiency for the business owner. The process gap reveals itself through what's missing: no one owns the comprehensive client relationship or envisions the client's lifecycle trajectory and long-term value. No process ensures holistic needs assessment. No system orchestrates integrated solution delivery. None of the colleagues are conversationally competent to talk to the business owner holistically. Most critically, no one is held accountable when $250M in proceeds walk out the door — because no one was responsible for the integrated relationship in the first place.

The True Cost of Process Failure

When banking processes prioritize departmental efficiency over client experience, the financial and strategic consequences cascade through the organization in ways that most senior executives never fully quantify. The real cost isn't just the immediate lost revenue — it's the compounding effect of relationship deterioration that destroys decades of investment and future potential. Consider the relationship deterioration that inevitably occurs when clients encounter impersonal interactions where they feel like account numbers rather than valued partners. Each departmental handoff becomes a transactional moment where the client must re-establish their story, re-explain their needs, and re-evaluate their commitment to the banking executives underestimate how these process failures create long-term competitive disadvantages. Independent advisory firms systematically target business owners who express frustration with their bank's fragmented approach, positioning themselves as the comprehensive solution banks claim to be but fail to deliver. Technology-enabled competitors leverage superior client experience to overcome traditional banking advantages, while credit unions and community.

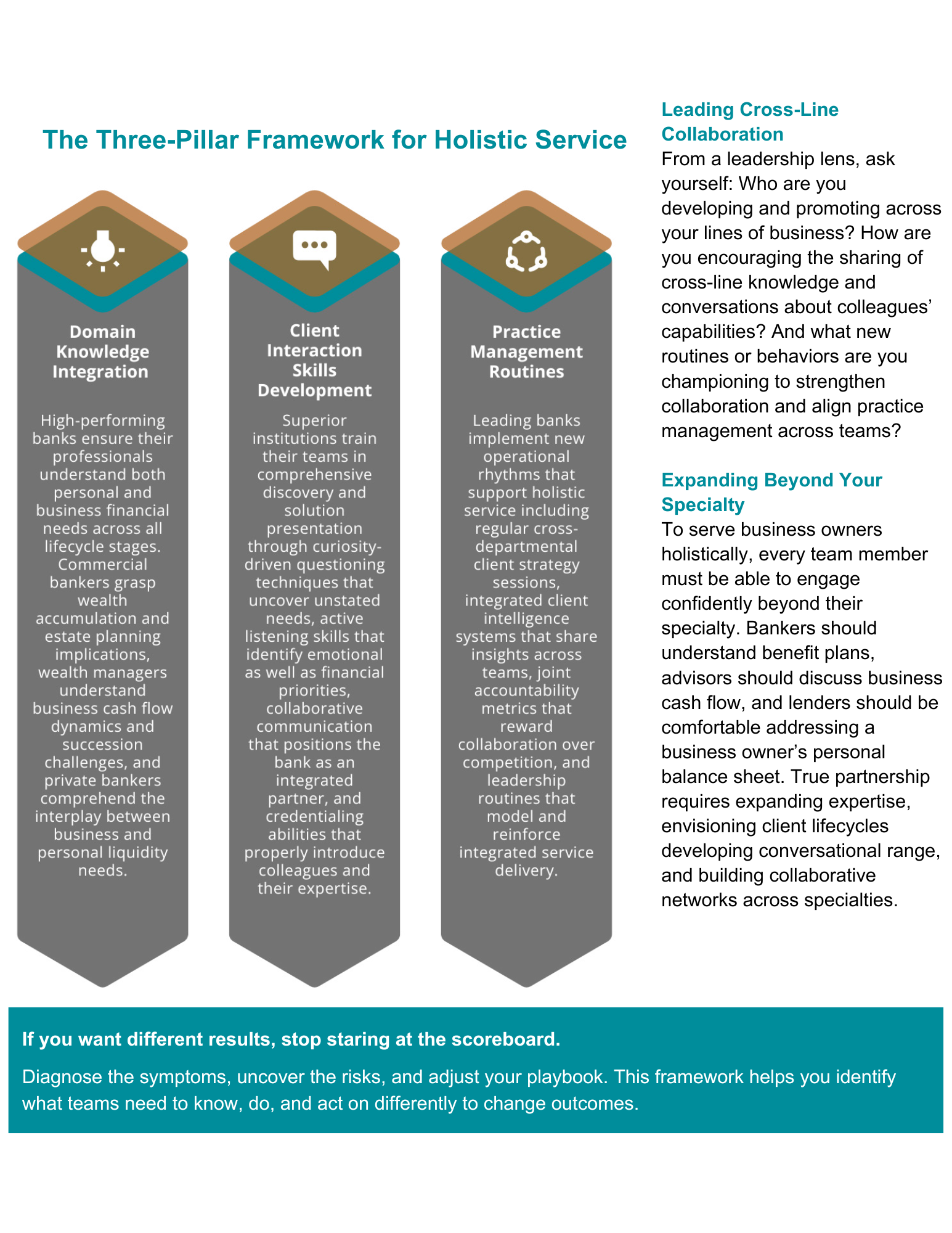

What High-Performing Institutions Do Differently

Leading banks are beginning to recognize that process transformation requires more than organizational restructuring — it demands fundamental changes in how teams operate, communicate, and serve clients.

The Culture Imperative: Senior Leaders as Culture Architects

The most successful transformations begin with senior executives who recognize their role as culture architects. They understand that process change without culture change inevitably fails, and that culture transformation requires consistent, visible leadership commitment over extended periods. These leaders ask fundamentally different questions about their organizations. Instead of focusing solely on departmental performance metrics, they examine the daily routines, behaviors, and interactions that create client experience. They want to know how often wealth management and commercial lending leaders meet to discuss shared clients, what routines exist between treasury management professionals and private bankers, and how cross-departmental collaboration permeates senior staff meetings. Most importantly, they recognize that sustainable culture change requires developing new coaching capabilities throughout the management ranks, ensuring that middle managers can effectively guide front-line professionals in comprehensive discovery, collaborative solution development, and integrated relationship management.

Measuring What Matters: KPls That Drive Cultural Change

Traditional banking metrics reward departmental performance through individual advisor production goals, product-specific sales targets, and cost center profitability analysis. These measurements actively work against comprehensive service delivery by creating internal competition rather than collaboration. Senior executives serious about culture transformation must ask themselves challenging questions about what they're actually measuring and rewarding. The development of new performance frameworks requires careful consideration of your organization's current culture and readiness for change. Some institutions can immediately implement comprehensive relationship metrics, while others need transitional measurements that gradually shift behavior toward collaborative service delivery. The key is ensuring that whatever metrics you choose actively support the culture you're trying to create rather than reinforcing the departmental mindset you're trying to change.

Competitive Reality: Windows Close Quickly

The financial services landscape is shifting rapidly, and the window for banks to establish comprehensive service delivery advantages is narrowing. Business owners increasingly expect their financial partners to understand their complete situation and provide integrated solutions, not departmental products. This expectation shift creates immediate competitive pressure as RIAs, family offices, and fintech companies capture market share by providing the comprehensive experience that traditional banks promise but fail to deliver. Recent regulatory changes favor integrated service models that truly serve client interests rather than product sales quotas, creating an environment where comprehensive service delivery becomes not just preferred but practically required for competitive success. The institutions that successfully transform their culture and processes for holistic business owner service will capture significant competitive advantages that compound over time. Market differentiation becomes genuine when banks can deliver true comprehensive service rather than coordinated departmental efforts.

This differentiation supports premium pricing power as clients pay more for integrated solutions that address all their needs rather than piecemeal products. The relationship stickiness that results from comprehensive service makes it much harder for competitors to disrupt established partnerships, while satisfied business owner clients become powerful referral sources for similar high-value prospects. Perhaps most significantly, top professionals prefer working in organizations that enable them to truly serve clients rather than just sell products. Banks that create cultures supporting comprehensive service delivery will attract and retain the talent necessary to compete in an increasingly sophisticated marketplace. The first-mover advantage window remains open, but not indefinitely. Banks that continue delaying culture and process transformation while competitors demonstrate superior comprehensive service capabilities will find themselves acquiring one business owner relationship while losing established ones — a loss their billion-dollar blind spot makes invisible until it's irreversible.

The Leadership Challenge: Recognizing the Problem

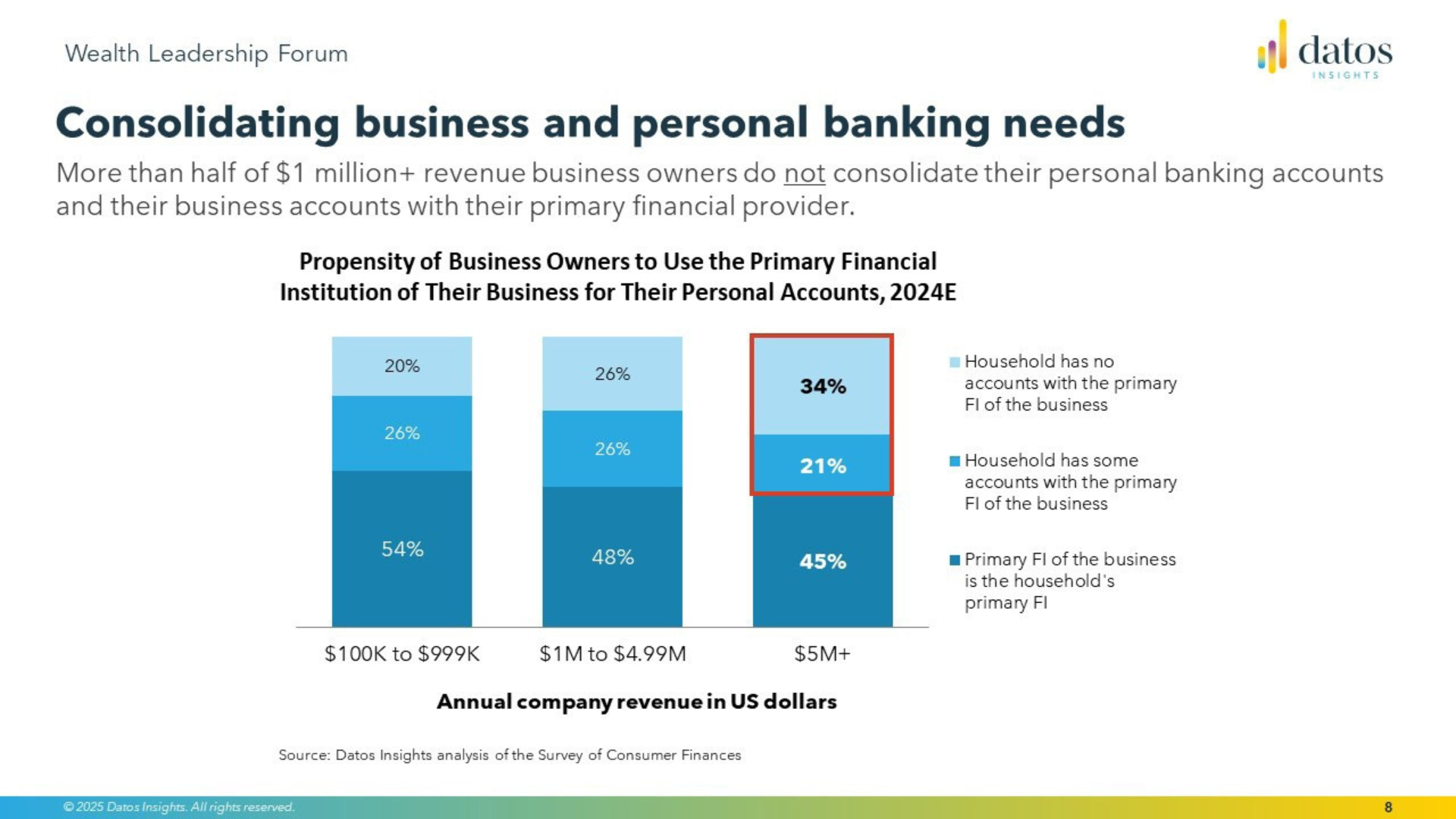

The most difficult aspect of addressing this challenge isn't developing solutions — it's getting senior executives to recognize the problem exists at all. Many banking leaders believe they already serve business owners comprehensively because they have all the necessary departmental capabilities and documented "referral" processes. Simply having the experts and resources is necessary, but it's not sufficient if the clients aren't leveraging them. Datos Insights' research (see Figure 7) reveals that 55% of business owners with $5 million+ in revenue maintain their household accounts elsewhere or only partially consolidated with their business's primary bank. These aren't marginal relationships—they represent the highest-value clients every bank claims to prioritize. Your most profitable clients have already voted with their wallets. The question is whether your organization will transform its culture to win them back. The question isn't whether you have the capability to serve business owners holistically — you do. The question is whether your current culture and processes actually deliver on that capability in ways that clients recognize and value. If business owners don't feel comprehensively served by your organization, then regardless of your capabilities, you're not serving them comprehensively.

The most revealing diagnostic questions focus on client experience rather than internal processes. When business owners describe their relationship with your bank, do they talk about a unified team that understands their complete situation, or do they describe interactions with various departments that each handle different pieces? When they face complex financial decisions, do they instinctively call your bank first, or do they contact other advisors who they trust to provide comprehensive guidance? Senior executives who recognize these patterns and commit to culture transformation will create sustainable competitive advantages with their most profitable client segment: business owners. Those who continue believing that departmental excellence equals comprehensive service will watch their most valuable relationships migrate to competitors who understand what business owners really want: a unified team that knows them, serves them holistically, and partners with them at every stage of their journey. The choice facing banking leadership is straightforward but not simple: transform your culture to deliver the comprehensive service that business owners need and expect, or continue watching your most profitable clients build their wealth elsewhere.

The Moment of Truth

The evidence is overwhelming. Banks possess every capability necessary to serve business owners comprehensively, yet most are losing these relationships to more agile competitors. The difference isn't capacity, technology, or resources.

It's culture and the processes that culture creates. Business owners don't want to be handed off between departments. They don't want to repeat their story to multiple advisors. They don't want product presentations when they need strategic guidance. They want what every successful entrepreneur deserves: a unified team that understands their complete situation and provides integrated solutions that address their real needs. The transformation required isn't technological or structural — it's cultural. Senior executives must become culture architects, designing organizational environments where comprehensive service delivery becomes natural rather than exceptional. This means changing how teams collaborate, how performance is measured, how professionals are developed and coached, and how client relationships are managed. The business owner market demands this transformation now. Client expectations have permanently shifted toward integrated service delivery, competitive pressure from comprehensive service providers continues intensifying, and regulatory environments increasingly favor client-centric approaches over product-centric ones. Banks that successfully make this cultural transformation will capture competitive advantages that compound over decades. They'll command premium pricing for integrated solutions, develop unbreakable client relationships, attract top talent who want to serve clients comprehensively, and build referral networks that drive sustained growth. Banks that delay or avoid this transformation will continue watching their most profitable relationships disappear to competitors who understand what comprehensive service actually means. The time for incremental improvement has passed.

The business owner market demands cultural transformation, and banking executives who recognize this reality and act decisively will determine their institution's competitive position for the next generation. Your business owner clients are waiting for you to become the comprehensive partner you claim to be. Your competitors are already working to capture the relationships you're not serving holistically. Your shareholders expect you to maximize the value of your most profitable client segments. The question isn't whether comprehensive service delivery is important — business owners have already answered that question by choosing providers who serve them holistically. The question is whether your organization will transform its culture to deliver what your clients need, or whether you'll continue executing processes designed for your convenience rather than their success. The moment of truth has arrived. What will your leadership team choose to do?