-

- Author

- Cannon Financial Institute

-

- Published

- March 30, 2026

Articles

How the Greatest Wealth Transfer Will Affect Gen X, Millennials and Gen Z

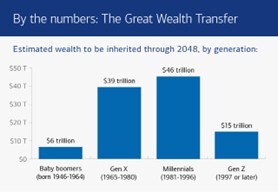

Over the next two decades, an estimated $124 trillion will pass from older generations to Gen X, Millennials and Gen Z. This is a historic shift known as the Greatest Wealth Transfer. This change is not just about wealth, but also about how younger investors think about money, how they invest and plan for the future. Financial advisors and estate planners should educate clients, build trust and develop personalized strategies that meet the specific needs of each generation.

At Cannon Financial, we are aware that the “Greatest Wealth Transfer” is a defining moment for financial advisors and wealth management firms. According to Merryl Lynch, over the next two decades, an estimated $124 trillion will move from older generations to younger ones, with most of it going to Gen X, Millennials and Gen Z.

What you have to explain to clients is that it’s not just about large amounts of money changing hands. It also affects how people think about money. For example, it’s a no brainer that younger investors have different goals, aspirations and preferences than older ones. It means that they want different types of advice, strategies and interactions with their financial guide. For estate planners this creates big opportunities to serve new clients, but they should also adjust their approach to meet these new expectations.

A Generational Shift in Wealth—and Mindset

Most of this wealth will come from baby boomers, with about $106 trillion expected to go directly to heirs and the rest to charitable causes (Bank of America). Sources suggest that roughly half of this transfer will come from high-net-worth households, even though they represent a small fraction of the population. And as we all know, wealth is becoming more concentrated and usually compounds at the top.

But here’s where things get interesting: the next generation doesn’t think like the last one. This is another important pointer every advisor should keep in mind.

Younger investors tend to be quite skeptical of traditional portfolios consisting of stocks, bonds and real estate. Many believe these alone won’t deliver above-average returns anymore. Instead, they’re exploring alternative investments such as private equity or digital assets. Many of them are trying to build their own businesses, which is a topic of a totally different conversation.

For advisors, this signals a clear shift. In other words, a one-size-fits-all investment approach won’t resonate. Client conversations should no longer be fully focused on traditional asset allocation but expand into broader, more flexible strategies. Make sure you are well-equipped to proceed down that road.

Being prepared is key

Evidence shows that despite the massive wealth heading their way, many Millennials and Gen Z investors aren’t fully prepared to manage it. No wonder they need steady guidance from a well-trained estate planner.

According to Merrill Lynch, a relatively small percentage report strong financial health or confidence in long-term planning. Even fewer feel capable of setting and sticking to a financial plan. Retirement remains a major concern across generations, but younger investors often lack the know-how and discipline to address it effectively.

Once again, this predicament creates both a challenge and an opportunity.

Advisors are no longer just investment managers — they are educators, coaches and long-term partners. Helping clients understand how to manage, preserve and grow wealth will be just as important as helping them acquire it (Guardian). And in order to properly educate clients, estate planners should get the education and knowledge THEY need to steer clients in the right direction.

Rethinking Planning Strategies

Here is another crucial detail to keep in mind. The Great Wealth Transfer highlights the importance of planning on both sides: those passing down wealth and those receiving it.

Of course we should mention that taxes are a critical piece of the puzzle. Without thoughtful planning, a big portion of transferred wealth can be lost.

As stated by Guardian, there are a few tools advisors should keep top of mind:

- Lifetime gift exemption: Allows individuals (and couples) to transfer substantial wealth over time without triggering taxes.

- Annual exclusion: Enables smaller, consistent gifts each year without using up your lifetime gift limit or paying gift taxes.

- Education and medical exclusions: Covering tuition or healthcare costs directly can transfer value without tax consequences.

Now do your clients know this information? If they don’t, you have your work cut out for you as a financial educator.

The Human Side of Wealth

This can come as a big surprise to many people, including some financial advisors but….even high-net-worth clients can lack confidence, react emotionally to market swings or go without a financial professional. According to Yahoo Finance, only 50% of high-net-worth individuals say they do not panic when their investments “hit a bad patch”. Nearly 47% of them do not even work with an advisor.

Younger generations also view wealth differently – they usually prioritize experiences, entrepreneurship, social impact or purpose-driven investing. Advisors need to go beyond numbers—understanding values, goals, and motivations is key to building trust. Personalization matters: Gen X may focus on retirement and preservation, Millennials on wealth-building and major life goals and Gen Z on understanding the basics of money management.

Final Thoughts:

The Greatest Wealth Transfer is more than just money changing hands—it’s a shift in mindset, goals and expectations across generations. Advisors who patiently educate clients, personalize strategies and build multigenerational relationships are best positioned to guide families through this historic transition. Success comes from combining knowledge, empathy and highly customized planning for each generation.

Source: Cerulli Associates, “The Cerulli Report: U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2024

FREQUENTLY ASKED QUESTIONS:

1. Why is the Greatest Wealth Transfer important for advisors?

It’s not just a transfer of assets—it’s a transfer of relationships. Advisors who connect early with heirs, educate them, and personalize strategies can maintain and grow client relationships across generations.

2. How do Millennials and Gen Z differ from older generations in handling wealth?

They tend to prioritize experiences, entrepreneurship, philanthropy, and alternative investments, and often lack foundational financial knowledge and long-term planning experience.

3. What tools can help with effective wealth transfer?

Key tools include the lifetime gift exemption, annual exclusion, education and medical exclusions, and the marital deduction—all of which help transfer wealth efficiently while minimizing taxes.